Understanding Your Situation Net Worth: More Than Just A Number

Have you ever paused to think about your finances, not just as a set of numbers on a spreadsheet, but as something deeply connected to what's happening around you? It's a bit like looking at a house; you see its walls and roof, yet its true value, its feeling, really comes from where it sits, the neighborhood, and what's going on inside. Your net worth, too, is very much tied to its surroundings, its current conditions.

For many, net worth seems like a straightforward calculation: what you own minus what you owe. But, that's really just one piece of the puzzle, isn't it? The true picture, what we call your "situation net worth," captures so much more. It's about recognizing how your financial standing is shaped by the present moment, the broader economic currents, and even where you happen to be.

So, we're talking about a dynamic view of your financial health, one that considers the conditions that exist at a particular time. This isn't just about assets and liabilities; it's about how those things are influenced by the world around you, and how they might shift with changing circumstances. It’s a very practical way to look at your money.

Table of Contents

- What Exactly is Your Situation Net Worth?

- Why Your Current Circumstances Matter So Much

- Figuring Out Your Situation Net Worth: A Practical Guide

- Real-World Examples of Situation Net Worth in Action

- People Often Ask About Situation Net Worth

- Moving Forward with Your Financial Picture

What Exactly is Your Situation Net Worth?

The idea of "situation net worth" really broadens how we think about our money. When we talk about a "situation," we often mean the way something is placed in relation to its surroundings, or the set of things that are happening and the conditions that exist at a particular time. So, your situation net worth isn't just a static number. It's a living snapshot, one that considers your financial position within its current environment, like your home being situated on a hill with a beautiful view.

It includes your assets, like your savings, investments, and property, and your liabilities, such as loans and credit card balances. Yet, it also takes into account the wider context. This can mean the job market where you are, the overall economy, or even specific personal happenings that affect your money. It's a rather more complete way of looking at things, you know?

Sometimes, the word "situation" is used to refer generally to what is happening in a particular place at a particular time, or to what is happening to you. This is precisely what we're getting at with situation net worth. It’s about how your money is positioned given all the things going on, right now, in your life and the world around you. It’s a bit like saying, "The company is in a crisis situation," meaning its current state is influenced by specific, challenging circumstances.

Beyond the Numbers: A Broader View

Thinking about your situation net worth means going beyond just adding up your bank accounts and subtracting your debts. It's about considering the "deal," the "status," or the "state" of your financial world. For instance, your home's value might be high on paper, but if the local job market is struggling, that could affect how quickly you could sell it, or what you might get for it. This broader view helps you see potential risks and opportunities that a simple balance sheet might miss.

It’s about recognizing that your financial picture is always moving, always adapting to what’s happening. A critical set of circumstances, for example, like a sudden market downturn, can really change how your net worth looks, even if the basic numbers haven't moved yet. This deeper understanding helps you make better choices, too, as a matter of fact.

This perspective also helps us avoid using "situation" in ways that are a bit imprecise. Instead of just saying "people in a job situation," we can think about how that job situation specifically affects their current financial standing, their ability to save, or their debt load. It provides a more meaningful context for your money, actually.

Why Your Current Circumstances Matter So Much

Your financial health is not just about the money you have or owe; it's deeply connected to the world you live in. The conditions that exist at a particular time, the set of things that are happening, these all play a big part in shaping your true financial standing. It’s not just a number, but a reflection of your current environment and experiences.

Consider how your current job, or even the industry you work in, affects your income and your ability to save. If your industry is booming, your earning potential might be higher, and your job more secure. On the other hand, if your industry is facing challenges, your income might be less predictable, which in turn impacts your overall financial picture. This is a very real example of how your situation influences your wealth, you know?

Even something like your health, or the health of family members, can greatly influence your situation net worth. Unexpected medical bills, for instance, can quickly change your financial status, requiring you to dip into savings or take on debt. These personal circumstances are just as important as market trends when we think about our true financial standing, so.

Economic Shifts and Your Wealth

The economy is like a massive, constantly moving ocean, and your net worth is a boat sailing on it. When the economy is strong, with low unemployment and rising wages, your investments might grow, and your job prospects feel secure. This positive "situation" can help your net worth increase. However, when economic conditions get tough, like during a recession, things can look very different. Stock markets might fall, property values could drop, and job security might lessen. This is where the concept of "situation net worth" truly shines, as it helps you see how these broader currents affect your personal financial scene.

Think about inflation, for example. If prices are rising quickly, the purchasing power of your cash savings goes down, even if the number in your bank account stays the same. This means your "situation net worth" might be less robust than it appears on paper. It's about understanding the real value of your money in the current economic state, which is a bit more nuanced than just looking at the raw figures.

Interest rates are another big one. When rates go up, the cost of borrowing money increases, making loans more expensive. This can affect your mortgage payments or the interest on your credit cards, which impacts your cash flow and, by extension, your ability to save or pay down debt. On the flip side, higher interest rates can mean better returns on savings accounts, which is a positive for some aspects of your wealth. These are all part of the "conditions that exist at a particular time" that shape your financial story, naturally.

Personal Life Events and Their Financial Ripples

Life is full of unexpected turns, and many of these events have a direct impact on your financial standing. Getting married, having children, buying a home, or even going back to school can significantly change your income, expenses, and assets. These aren't just minor gaffes; they are major shifts that create a new "situation" for your net worth. For instance, starting a family often means new expenses, but it might also prompt you to think more about long-term savings and insurance, which is a really important shift.

Losing a job, facing a serious illness, or dealing with a natural disaster can also create a critical, problematic, or striking set of circumstances for your finances. These moments can force you to use emergency funds, take on new debt, or sell assets, all of which directly affect your net worth. Understanding this helps you prepare for the unexpected, and that's a key part of managing your money effectively, too it's almost.

On the brighter side, receiving an inheritance, getting a promotion, or selling a business can dramatically boost your net worth. These positive events also change your financial situation, perhaps allowing you to pay off debt, invest more, or achieve long-held financial goals. It's about recognizing that your financial picture is always in motion, shaped by the many things that happen in your life, you know.

The Place You Call Home

Where you live, your location or position with reference to environment, plays a surprisingly big part in your situation net worth. Housing costs, local taxes, job opportunities, and even the cost of everyday goods vary widely from one place to another. A building might be situated on the top of a hill, and that's its position or situation; similarly, your financial life is situated within a specific geographic area, and that matters a great deal.

For instance, if you live in a city with a very high cost of living, your income might need to be much higher just to maintain the same lifestyle as someone in a more affordable area. This impacts your ability to save and invest, which directly affects your net worth over time. The situation of the house allowed for a beautiful view, and the situation of your home allows for certain financial realities, you see.

The local job market in your area also really influences your income potential and job security. If your skills are in high demand locally, you might command a higher salary. If not, finding work or advancing your career might be tougher. All these regional factors contribute to the overall "conditions that exist at a particular time" for your financial life. It's a very practical consideration, really.

Figuring Out Your Situation Net Worth: A Practical Guide

Getting a handle on your situation net worth means doing a bit more than just simple arithmetic. It involves taking a thoughtful look at your assets and liabilities, then layering on the context of your current life and the world around you. This approach helps you see the bigger picture, the "state" or "picture" of your finances, you know.

It’s about asking yourself not just "What do I have?" but "How stable is what I have, given everything else?" This way, you move past a simple snapshot and start to build a more complete story of your financial health. It’s a very useful exercise, actually.

This process also encourages you to think about potential future scenarios. What if your job situation changes? What if the housing market shifts? By considering these possibilities, you can better prepare and make your financial standing more resilient. It’s all about being proactive, more or less.

Step One: The Basic Calculation

First things first, you need to calculate your traditional net worth. This is your foundation. List all your assets: cash in bank accounts, investments (stocks, bonds, mutual funds), retirement accounts (401k, IRA), real estate (home value), vehicles, and any other valuable possessions. Then, list all your liabilities: mortgage, car loans, student loans, credit card debt, and any other money you owe. Subtract your total liabilities from your total assets. That number is your basic net worth. This is the starting "position" or "footing" of your financial situation, so.

You can use a simple spreadsheet or even a pen and paper for this. The goal here is just to get a clear, current number. Don't worry about the "situation" part just yet; we'll add that in the next step. This initial calculation gives you a clear baseline, which is really helpful, you know.

Make sure you're using current values for your assets, especially things like investments and real estate, which can change quickly. For example, you might check a site like Zillow for an estimate of your home's value, or your investment accounts for up-to-date balances. This ensures your basic calculation is as accurate as possible, too.

Step Two: Adding the "Situation" Layer

Now, this is where the "situation" really comes in. Once you have your basic net worth number, think about the conditions that exist at this particular time that might affect it. Ask yourself questions like:

- **Job Security:** How stable is your current job? Is your industry growing or shrinking? Could a job loss significantly impact your income and ability to pay debts?

- **Economic Outlook:** What are the current trends in the economy? Is inflation high? Are interest rates rising or falling? How might these affect your investments or the cost of your debts? You can find a lot of information on this from reliable sources, perhaps by looking at reports from financial institutions or government agencies, which is a good idea.

- **Local Market Conditions:** How is the housing market doing in your area? Are property values increasing or decreasing? What about the local job market?

- **Personal Health & Family:** Are there any health concerns for you or your family that could lead to unexpected expenses? Are there any big life events coming up, like starting a family or planning for college, that will change your financial picture?

- **Emergency Fund:** Do you have enough cash set aside to cover several months of living expenses if something unexpected happens? This acts as a buffer against a "crisis situation" for your finances.

Consider how these factors create the "scene" or "picture" of your current financial standing. For instance, if your net worth includes a lot of stock in one company, and that company is facing a "crisis situation," your true financial stability might be less than the numbers suggest. It’s about looking at the "posture" of your wealth, if you will, which is a bit more involved than just the numbers.

This isn't about changing the numbers on your balance sheet directly, but about adding a layer of understanding and context. It helps you see the potential vulnerabilities or strengths in your financial setup, which is really useful for planning. It's a very practical way to approach your money, honestly.

Step Three: Regular Check-ins

Your situation net worth isn't a one-time calculation. Just like the general "situation" in the world changes, so too will your personal financial situation. It's a good idea to revisit this assessment regularly, perhaps every six months or once a year, or whenever a major life event occurs. This helps you stay aware of shifts and adjust your financial plans accordingly.

Keeping an eye on economic news and local market trends can also help you anticipate changes. If you hear about potential interest rate hikes, for instance, you might consider paying down variable-rate debt faster. This regular review helps you keep your financial "state" in good order, and that's pretty important, you know.

By making this a habit, you'll gain a deeper understanding of your financial resilience and be better prepared for whatever comes your way. It’s a bit like checking the weather before you go out; you know what to expect and how to dress. This is a simple, yet powerful, way to manage your money, you see.

Real-World Examples of Situation Net Worth in Action

Let's look at a few common scenarios to really bring the idea of "situation net worth" to life. Imagine Sarah, who has a net worth of $200,000. On paper, that looks pretty good. However, her "situation net worth" might tell a different story. What if $180,000 of that is tied up in her home, which is located in an area with a declining job market and a potential housing bubble? Her liquid assets are low, and her main asset is in a risky "situation." This means her true financial flexibility is quite limited, even with that seemingly solid number.

Then there's David, whose net worth is $100,000. This is lower than Sarah's, but his "situation net worth" might be stronger. Perhaps he has $50,000 in a diversified investment portfolio, $30,000 in a high-yield savings account, and only $20,000 in home equity. He also works in a very stable, growing industry. His "deal" or "status" is one of greater liquidity and less exposure to specific market risks. He's in a better "state" to handle unexpected events, you know, which is a really good thing.

Or consider Maria, who recently had a baby. Her basic net worth might not have changed much initially, but her "situation net worth" has shifted significantly. She now has increased expenses for childcare and baby supplies, and perhaps a reduced income if she's on maternity leave. This new "set of things that are happening" means her financial picture, her "scene," is much tighter, even if the numbers on paper look similar to before. It's a very common scenario, actually.

These examples show that the raw number is only part of the story. The context, the "conditions that exist at a particular time," truly defines your financial standing. It’s about seeing the whole picture, the "picture" of your financial health, rather than just isolated figures. This perspective helps you make more informed choices, which is pretty important.

People Often Ask About Situation Net Worth

When we talk about your financial health, some questions come up a lot. Here are a few that people often ask, helping to clear up what we mean by "situation net worth."

What is the difference between net worth and financial situation?

Net worth is a specific calculation: your assets minus your liabilities. It's a number. Your "financial situation," however, is a much broader concept. It includes your net worth, but also considers your income, expenses, cash flow, debt-to-income ratio, and your ability to meet financial goals. It's the overall "state" of your money life, including how your money moves and how secure it feels. So, net worth is a part of your financial situation, but not the whole story, you know.

How do current events impact my net worth?

Current events, like economic changes, political developments, or even global health concerns, can greatly affect your net worth. For example, a stock market downturn can reduce the value of your investments, while rising interest rates can make your debts more expensive. A strong job market, on the other hand, might increase your income and ability to save. These events create the "conditions that exist at a particular time" that shape your financial picture, very truly.

Can my location affect my net worth?

Absolutely, your location or position with reference to environment can significantly impact your net worth. Housing costs, local taxes, job opportunities, and even the cost of living vary greatly by region. Living in a high-cost-of-living area might mean you need a higher income to save money, while a strong local job market could boost your earning potential. The "situation of the house" affects its value, and the "situation of your life" affects your financial standing, too.

Moving Forward with Your Financial Picture

Understanding your situation net worth is a powerful step towards feeling more in control of your financial life. It helps you see beyond the simple numbers and truly grasp the "conditions that exist at a particular time" that shape your wealth. This perspective encourages you to be proactive, to think about potential changes, and to make choices that build resilience into your financial future.

By regularly assessing your financial "state" within its broader context, you can better prepare for life's ups and downs. This isn't about being anxious; it's about being aware and empowered. It's about knowing your financial "story" in a deeper, more meaningful way, which is a very good thing, you know. To learn more about personal finance basics on our site, you can explore our various resources.

Keep in mind that your financial journey is unique, and it's constantly evolving. Staying informed about economic trends and being mindful of your personal circumstances will help you adapt and grow your wealth. If you're looking for more ways to manage your money, you might find some useful insights on this page financial planning tips. Remember, it’s all about seeing the full "picture" and making smart choices for your future, so.

For more detailed information on economic trends and their impact on personal finance, you might consider looking at reputable sources like the Federal Reserve's website, which offers a lot of data and reports.

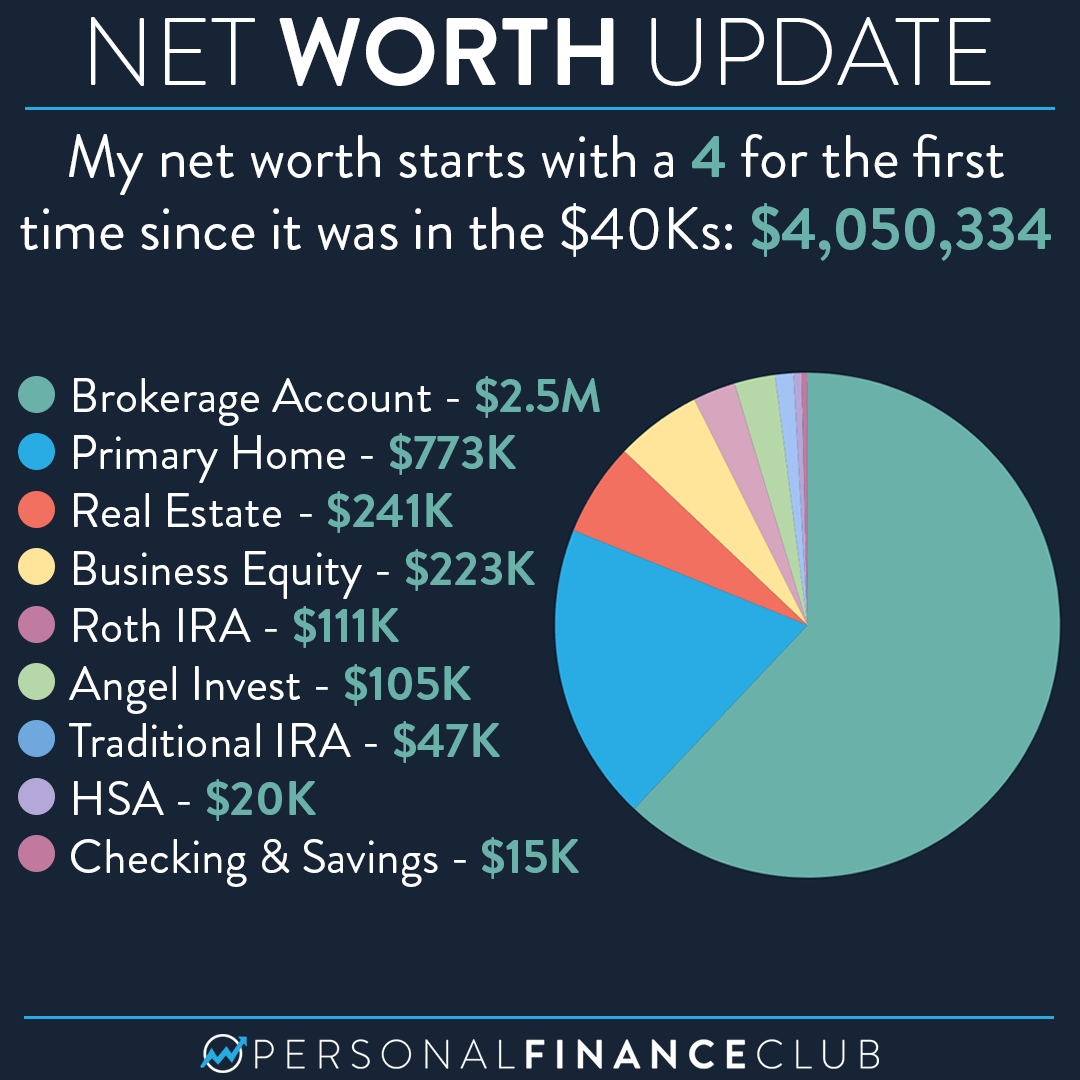

My $4 million net worth breakdown! – Personal Finance Club

NET WORTH OF A LIFE

Mike The Situation Sorrentino Net Worth - Net Worth Post